Hundreds of thousands of today’s service members face will have a critical big decision to make during the next year that could have a huge impact on their future financial security: Whether to opt into the new military retirement system or stick with the traditional one.

Signed into law in November, the new retirement benefit will mean promises smaller pension checks but include promises to give all troopcash contributions to the ir individual investment accounts of all troops.

It's the biggest change in decades for military compensation. For the first time, the military will offer some limited retirement benefit, similar to 401(k) contributions, to troops who separate before reaching 20 years of service. Historically those non-career service members — more than 80 percent of the force — received no retirement benefit.

Officially the new retirement system takes effect Jan. 1, 2018. After that, all troops coming out of boot camp will be automatically enrolled in required to accept the new benefit as the traditional pension plan is phased out.

Yet for today’s troops, and anyone who joins during the next two years, the new law includes a grandfather clause that will allow them to choose to remain keep them under the traditional all-or-nothing retirement system. if they choose.

The Defense Department plans to roll out a forcewide education program later this year to give troops the details on the new benefits and also provide financial literacy training to help them individuals make key decisions like how much personal basic pay to allocate to retirement savings accounts and where to invest it.

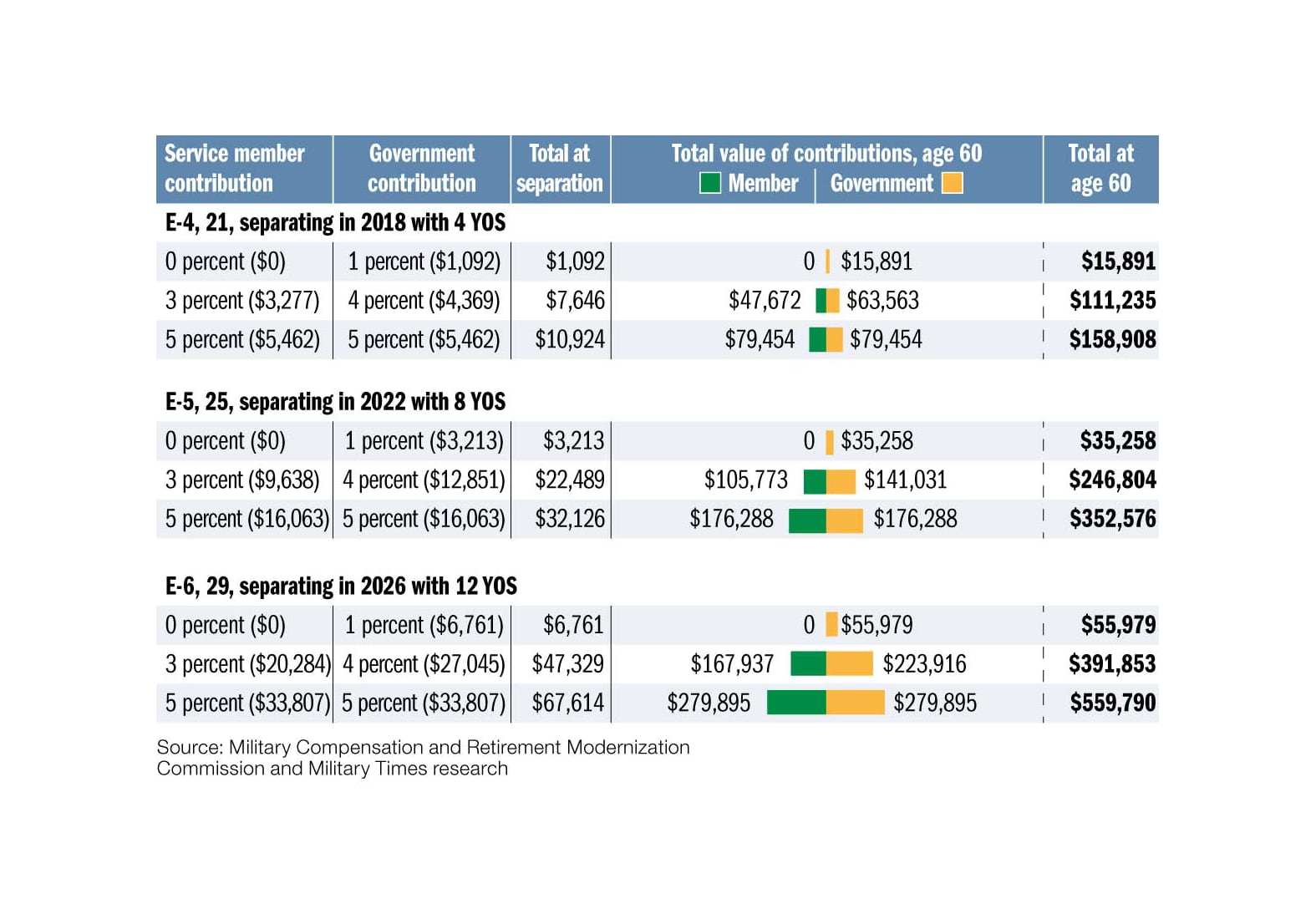

This chart gives a hypothetical look at how the new retirement system would work for six enlisted members if it had taken effect in 2015.

Photo Credit: John Bretschneider/Military Times

Despite years of skepticism, the new benefit looks like a potentially pretty good deal ((financial experts say???)) for many of today’s younger troops and the Pentagon expects thousands of service members to voluntarily waive their right under a grandfather clause to stick with the traditional system.

There’s an immediate incentive: Troops who opt in will begin receiving monthly cashmatching contributions — ranging from 1 percent to 5 percent of monthly basic pay — into their portable individual investment account that they own outright after just two years of service.

The new system caps years of heated debate over the future of military retirement. And the final outcome is vastly different from the initial proposals that would have eliminated the fixed-income pension entirely and gutted the real value of the benefit. Those proposals sparked outrage and were ultimately rejected by the Pentagon as a major risk to retention and readiness.

Troops who entered military service before 2006 are not eligible for opting into the new system.

Photo Credit: Staff Sgt. Caleb Wanzer/Air Force

In fact, the new system does not really save much money for the Defense Department. Most of the reduced spending on smaller pensions will be offset by the cash contributions for the vast majority of the rank-and-file force.

"It's an incredibly generous deal," said Mackenzie Eaglen, a military personnel expert at the American Enterprise Institute. "By and large this is the establishment of a generous new benefit for a wide swath of people who were never going to get it in the past," she said.

Offering a side-by-side comparison of the two retirement systems is difficult because it hinges on big variables, such as future stock market returns and the extent to which individual service members contribute their own pre-tax money to their retirement account and are in turn able to draw on the matching government contributions.

Troops who entered military service before 2006 are not eligible for opting into the new system and, generally speaking, for those troops who have already clocked many years in uniform and are well on their way to reaching the 20-year retirement threshold, the new system is not very attractive because they have far fewer years to accrue monthly cash contributions and let those grow with compound interest over time. ((growing with compound interest but also due to investment results???) That seems like the same thing to me, but I removed that phrase bc its not necesary//andrew)

Yet for troops who are early in their careers, especially the several hundred thousand who are first-term enlistees or junior officers, the question is more complex, experts say.

"This decision likely will depend on service members' answers to several questions. First, and most importantly, what is the likelihood that the service member will make the military a career and stay at least 20 years?" said Jim Grefer, a military personnel expert at the Center for Naval Analyses.

"Service members who are unlikely to stay to 20 years of service clearly would be better off under the new system," he said.

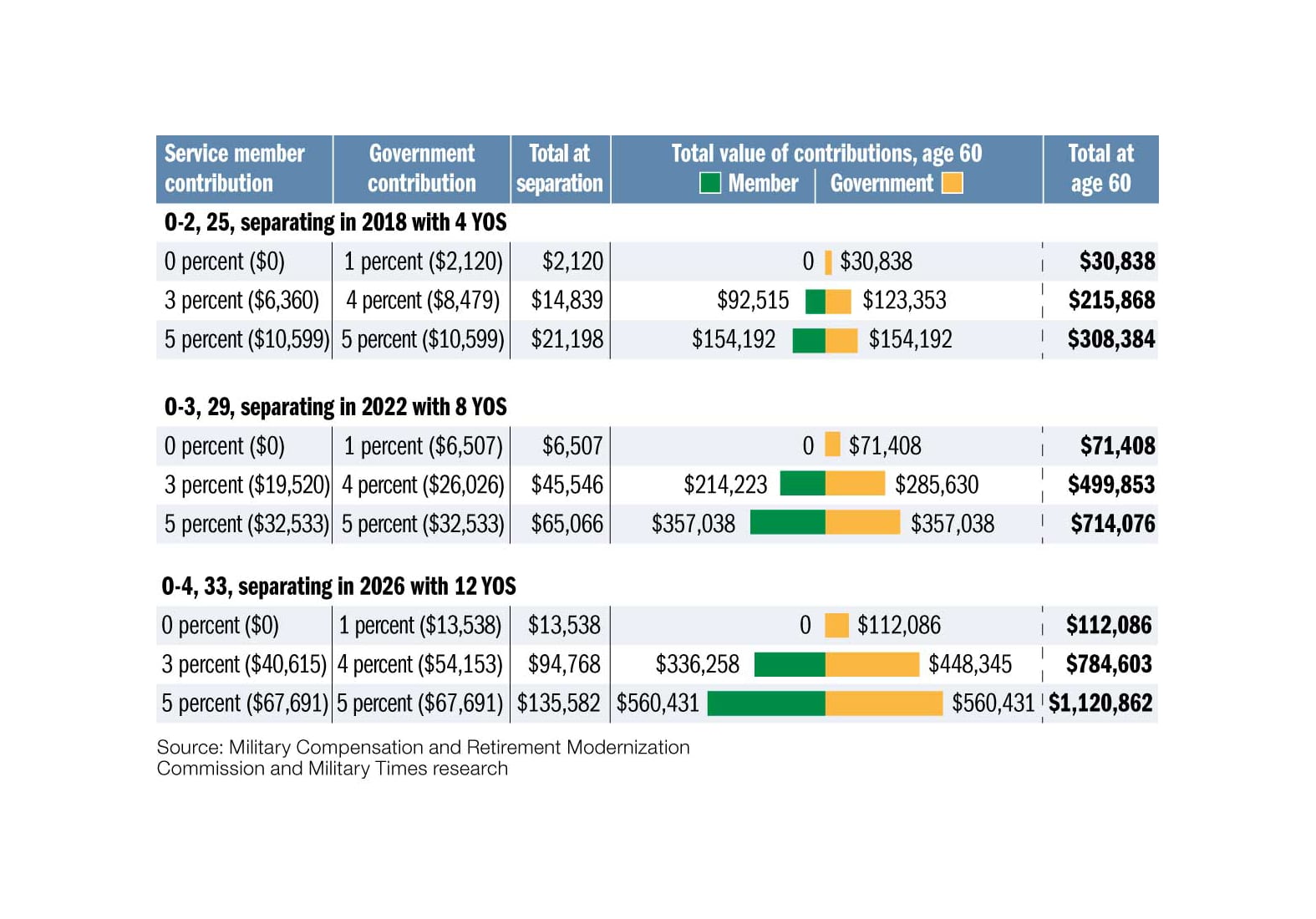

This chart gives a hypothetical look at how the new retirement system would work for six officers if it had taken effect in 2015.

Photo Credit: John Bretschneider/Military Times

For individuals who strongly believe they will remain in uniform for 20-plus years, exercising the grandfather clause and staying with the traditional benefit package might make more sense, he said.

They should focus on several key questions:

"Are they willing to sacrifice current spendable income by making contributions to their TSPs from their own pockets? And are they willing to accept the market risk inherent in TSP-type retirement accounts?" Grefer said

"If the answers are no, then they likely should stay in the current retirement system," he said.

Here are the details:

Under the new retirement system, military pensions will shrink by 20 percent, but otherwise will function the same as the current system, with i.e. the pension is earned after 20 years of active-duty service and with checks payable immediately upon separation.

Troops will receive a "continuation pay" upon reaching 12 years of service if they agree to a new four-year service agreement. Continuation pay will vary by career field but will be at minimum equal to 2.5 months of basic pay. These funds will be paid as cash, so service members can spend it — or invest it — as they wish. ((can it be rolled into the new investment plan??)it's cash so they can do whatever they want wit it, so yes//andrew)

The Defense Department will create an individual investment account, known as a Thrift Savings Plan, for all recruits showing up at boot camp. ((is this modeled after the existing TSP for federal employees - will it have the same investment options???) It is the TSP, it exists already but without matching contributions...the TSP is not new, just the payments//andrew) Troops will automatically receive monthly deposits equal to 1 percent of their basic pay. They Troops can select an investment fund and hope to accumulate market gains and interest over time as financial markets grow.

Ownership of the TSP accounts will be handed off to the individual troops after reaching two years of service. ((is there a major financial firm or firms that are managing these accounts and receiving fees for doing so???) It's the TSP and it offers investment in funds, not specific stocks, so yes, there are managers receiving fees, and it varies by which fund individuals select//andrew) Troops will be given incentives ncentivized to contribute their own money to the retirement account. Specifically, the Defense Department will offer a dollar-for-dollar match to individual contributions up to an additional 3 percent of pre-tax basic pay. (shouldn't this be 2 percent as those who contribute 3 percent get a 4 percent match???))

For troops opting to contribute 3 percent of their own basic pay, the Pentagon will contribute 4 percent, which would be i.e. the initial 1 percent automatic contribution plus and a 3 percent match. That means troops contributing 3 percent would sock away monthly pre-tax contributions the TSP account would receive month infusions equal to 7 percent of basic pay.

For those contributing to a TSP, there is the added benefit of reducing their taxable income. However, because the TSP offers investment funds, not specific stocks, standard maintenance fees will apply, and they will vary from fund to fund. ((RIGHT???) Yes, technically, though I dont think that's much real world benefit//andrew)

Additionally he Defense Department will match at 50 cents on the dollar troop contributions beyond 3 percent, up to 5 percent. The Defense Department will give troops 50 cents on the dollar if they tick up their own contributions to four or five percentSo to receive the maximum possible retirement benefit, troops should contribute 5 percent of their own basic pay and receive a 5 percent matching contribution from the government. ((not clear here ... we just said 50 percent on 4 or 5 percent - is it 50 percent on the 4 percent and a full 5 percent matching???) -- We will have a chart laying this out in detail. It is 50 cents on the dollar for the 4th and 5th percent ...meaning if you do 3 percent, you get 4 matching from the gov ...i.e. the 1 percent automatic and 3 percent dollar-for-dollar match. If you do four percent, the goverment will match 4.5 percent, i.e. 1 percent automatic and 3.5 percent match. sorry if I'm too lost in the details //andrew)

Troops are permitted to contribute more of their own money, ((any limit???)) but the government match is capped at 5 percent.

For those contributing to a TSP, there is the added benefit of reducing their taxable income. However, because the TSP offers investment funds, not specific stocks, standard maintenance fees apply, and they will vary from fund to fund.

Money deposited into a TSP is generally subject to a 10 percent penalty if withdrawn before the owner reaches age 59½. Taxes are deferred on contributions, payable upon withdrawal of funds.

Deadlines

After the official start of the new system in January 2018, today's troops will have 12 months to decide if whether they want to opt in.to the new system.

It all kicks off Jan. 1, 2018. In January 2018, theThat's when the Defense Department will begin distributing giving monthly retirement account contributions to the newest recruits arriving at boot camp as well as hose older troops who decide to opt into the new system as well as to troops already in the ranks who opt into the new system.

Opting in will require signing some basic paperwork. Those troops who joined the military before January 2018 will automatically remain under the current system unless they seek out the authorization forms for opting in.

Current plans call for giving current troops a 12-month window of time for opting in, so the last chance to sign up to participate in for the new benefit and its monthly cash contributions will be late December 2018.

Old bonuses

The law that fundamentally changes the retirement benefit is intended to dovetail with the longstanding system of special and incentive pays.

Re-enlistment bonuses for specific career fields, combat pays and special incentives for high-demand skills such as like proficiency in foreign languages or medical specialties training will continue to be a key device for the services to retain talent and shape the force.

"The new system isn’t meant to dislodge the existing ‘S & I’ pays," said James Hosek, a military personnel expert with the Rand Corp. whose research contributed to the development of the new retirement system. ((maybe a sitrep with this guy???))

Despite the pension’s reduction, its total value will continue to serve as an incentive for incentivize midcareer service members to stay in uniform. "The retirement benefit at 20 years of service is still substantial. It’s still a major draw," Hosek said.

THE FOLLOWING COULD BE REFERRED TO IN THE STORY AND SERVE AS A BREAKOUT SIDEBAR:

Lump sum

Among the biggest changes to the retirement benefit is a new option for troops leaving after 20 years of service to receive part of their pension benefit in the form of a "lump sum" cash payout.

Retiring service members will have the option of receiving their retirement benefit in the traditional form of monthly pension checks. Or, they can opt to receive 25 percent or 50 percent of that benefit in a single large cash payout upon separation in exchange for future years of reduced pension payments. (The lump-sum option reduces monthly pension checks only through the traditional retirement age, typically age 67, at which time all retirees will receive the full monthly pension benefit).

The lump-sum option in some ways will resemble today's "Redux" retirement option, in which troops can receive a $30,000 cash payment in exchange for reduced lifetime pensions. In most cases, the lump-sum payout will, after taxes, be worth less than $100,000.

Yet the precise amount of the lump-sum payments remains unclear. They won't be calculated by simply adding up the face value of pension payments. Rather, the calculations can rest upon a "discount rate," a device that financial professionals use to measure the current value of future payments.

Discount rates assume money today is more valuable than money tomorrow — akin to reverse interest rates, shaving money from the current value of a future benefit. The higher the discount rate applied, the lower the value of the lump sum payment today.

The law Congress passed leaves the details up to the Pentagon, which will face a big decision to make in setting that discount rate, one that will add or cut hundreds of thousands of dollars from individual troops' lump-sum options.

"That is going to be the largest point of contention. It's rife with missteps," said one defense official.

A key question is whether different service members will be offered different rates. Studies show enlisted troops are more eager to get money up front and therefore will accept a much bigger hit from the discount rate. But does that mean the DoD will take advantage of that and offer a better discount rate to officers?

If, hypothetically, studies show that the "grunts" in the combat arms career fields are willing to take the lump sum with a higher discount rate, will the Pentagon use that to craft the formal retirement benefits program and offer those troops smaller lump-sum retirement payouts?

"Do you split it by age? By pay grade By MOS?" the official said.

For troops who don't plan to make the military their career, the new retirement system would allow them to leave the service with money in a retirement account.

Photo Credit: MC2 Liam Kennedy/Navy

Critics of the lump-sum payout plan compare it to "pay-day lenders" and say it exploits individuals' desire to have cash now at the expense of long-term financial benefit.

An independent panel on military compensation initially floated the idea in a report to Congress in January 2015. The panel suggested it was a good option for retiring troops who want to buy a home, start a business or help send a child to college.

Last year the Defense Department officially opposed the idea ((whose idea???)added below//andrew) of a lump-sum cash payout, saying it was not a good deal for troops in most scenarios. The idea was first floated by the Military Compensation and Retirement Modernization Commission in a report to Congress last year.

Defense Department officials can kick that can down the road for a few years because it's unlikely that anyone will be completing their career and actually retiring under the new system for at least another 10 years.

Some defense officials are quietly hoping that Congress will revisit the new retirement law and eliminate that piece of the benefit package before any troops have an opportunity to exercise it.

"If we can get rid of it at some point it would be ideal," the defense official said.

Troops who opt into the new retirement system will face an array of new variables and decisions. What are the best investment fund options for a TSP account? How will financial markets impact the growth of retirement accounts? How much will the 12-year continuation pay actually be? Is the lump-sum option worth considering?

"It can be very complicated. But it can also come down to some very simple decisions, like contributions," said Beth Asch, a personnel expert with RAND.

"There are certain rules of thumb," she said. "Like if there is a match, do it."

Andrew Tilghman is the executive editor for Military Times. He is a former Military Times Pentagon reporter and served as a Middle East correspondent for the Stars and Stripes. Before covering the military, he worked as a reporter for the Houston Chronicle in Texas, the Albany Times Union in New York and The Associated Press in Milwaukee.