Navy Hospital Corpsman 2nd Class Ronald Rhea made his decision early on to opt in to the new Blended Retirement System.

He registered his choice on the first day he could sign up — Jan. 1 — and upped his contribution to the Thrift Savings Plan to 5 percent of his basic pay so that he could get the full Defense Department match.

“I can’t predict the future,” said Rhea, who is stationed at Naval Hospital Jacksonville, Florida. “I can’t necessarily say I’m in a situation where I’m guaranteed 20 years. I want to be able to leave, if forced to, with something.”

As an E5 with nine years of service, 5 percent of monthly basic pay is $156.29, so in 11 months that added up to $1,719 — and that amount is matched by DoD.

Combined, his and DoD’s contributions added up to $3,438 in the last 11 months.

With his previous contributions to and earnings in his TSP, he now has accumulated about $11,000.

RELATED

Although the opt-in decision can’t be changed now, he wanted to participate in the financial review to make sure he’s making the right moves now for his family’s future.

“I want to make sure the decisions I am making allow them the best opportunity for success,” said Rhea, who is married with two children, ages 8 and 5. “However, as a leader, I would also like to be a point of contact and be able to relay the information provided through me to those under me.

“I joined the military relatively late,” said Rhea, 39. “It can be a little bit concerning for an older sailor to see how retirement looks for them and works for them.”

Rhea is also using his military benefits in other ways with an eye toward the future, including pursuing a master’s degree. He also hopes to pursue a path of being commissioned as an officer.

“But in the event the military doesn’t work out, I want that degree in health care administration,” he said.

Other parts of the BRS also appeal to him, including the continuation pay when he reaches the 12-year-mark.

And if he does retire at the 20-year mark, taking a partial lump sum from his retirement could help tide the family over if he doesn’t find a job immediately, he said.

RELATED

He and his wife have been serious about paying down debt: They’ve paid off about $45,000 in student loan and other debt in the last year, now that she’s finished school and has been working.

“We’ve been living like I’m the only source of income,” he said, using her salary to knock down the debt.

After taxes, the Rheas’ income is about $9,000 a month, and their monthly expenses are about $3,000.

| Rhea’s situation | |

|---|---|

| Blended Retirement System? | Yes |

| Time in service | 9 years |

| Consumer debt | $23,000 two car loans $19,400 credit cards |

| Mortgage payment | $1,318 |

| Emergency fund | $4,500 |

| Retirement assets | TSP, $11,000 |

Reviewer: Andy Barnes, financial adviser with Navy Federal Financial Group.

Recommendations: To shore up their financial future, the Rheas should consider building their emergency fund to at least three months of living expenses, while simultaneously paying down their debt, Barnes said.

That’s about twice what their fund is now. These steps are a foundation for future finances.

In paying down the debt, they should first target the debt with the highest interest rate.

“After that debt is paid down, funnel [the payment] towards their next highest interest rate,” Barnes said.

The Rheas currently have three credit cards and two auto loans with interest rates higher than 6 percent.

HM2 Rhea should consider switching his Thrift Savings Plan contributions to the Roth option in the TSP, Barnes said, based on the family’s tax bracket.

Under the Roth option, you pay taxes on the contributions as you make them, and the earnings are tax free at withdrawal, as long as you meet certain Internal Revenue Service requirements.

Barnes noted that the Rheas should explore the retirement plan offered by Cheri Rhea’s employer and find out whether there is a company match.

If so, she should contribute at least enough to her retirement plan to get the company match. If there is no company match, she should still contribute at least 5 percent to start saving for her retirement, Barnes said.

Once they’ve paid off their consumer debt, Barnes said, the Rheas should increase their retirement savings to 10 percent to 15 percent of their income.

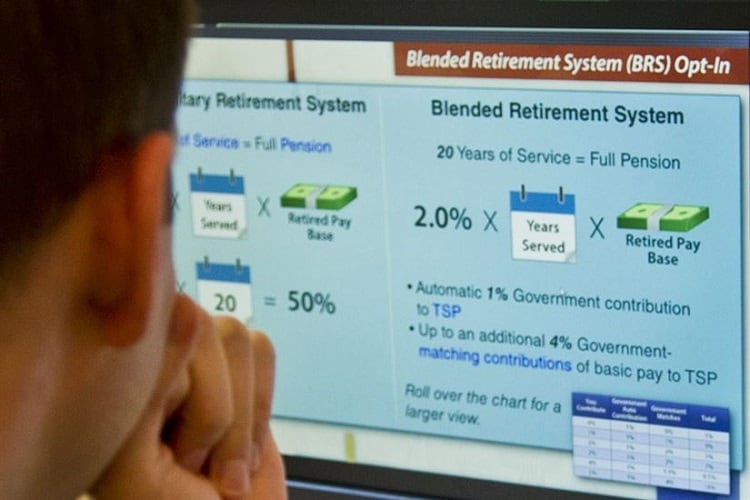

Right now, Rhea is contributing 5 percent of his basic pay to get the full match from DoD under the Blended Retirement System.

“If he does leave [the Navy] in the near future, the BRS would have benefited him, as his TSP and matching contributions are fully vested and transportable by transferring them into an IRA, should that suit him,” Barnes said.

Barnes said Rhea is aware of what he gave up in choosing the BRS over the legacy retirement plan, which could potentially provide a more comfortable retirement paycheck — 20 percent more — if he stays until he qualifies.

RELATED

What’s next: Rhea zoomed in quickly on Barnes’ advice about the debt with high interest rates.

“I wish we’d paid off our high interest rate debt first,” he said. “I crunched the numbers, and we could have saved $2,000” in interest by tackling that earlier.

“Getting rid of the debt with the highest interest rate first versus getting rid of the debt with the highest dollar amount makes a difference,” he said.

He also appreciated Barnes’ insight into the Roth option for his Thrift Savings Plan and is looking into that.

As Barnes advised, they’re continuing to focus on getting rid of the debt. Later, they’ll also look at increasing their retirement contributions and consider some investments outside the Thrift Savings Plan to add to their mix.

Cheri Rhea also has started contributing 5 percent of her salary to her 401(k) plan at work. Her company matches contributions of up to 3 percent of her salary.

“What resonated with me is what the Blended Retirement System provides, in regards to security for sailors going into what we do or do not know is going to be a guaranteed retirement,” Rhea said. “In speaking to junior sailors, I don’t think we realize that only 19 percent — 19 out of 100 military personnel — retire from the military.”

For him, it’s reassuring that they’ll have “that nest egg, that the military provides through the DoD Blended Retirement System contributions, even if I decide to get out at year 19 or 18 — or retire, for that matter.”

Karen has covered military families, quality of life and consumer issues for Military Times for more than 30 years, and is co-author of a chapter on media coverage of military families in the book "A Battle Plan for Supporting Military Families." She previously worked for newspapers in Guam, Norfolk, Jacksonville, Fla., and Athens, Ga.