For Air Force Capt. Brad Byington, crunching the numbers and taking a hard look at his career goals pointed to one path: He has decided to stick with the military legacy retirement system, rather than opting in to the new Blended Retirement System.

He volunteered to participate in the financial review, he said, to “validate my numbers as far as the retirement piece, and kind of validate a way forward for me.”

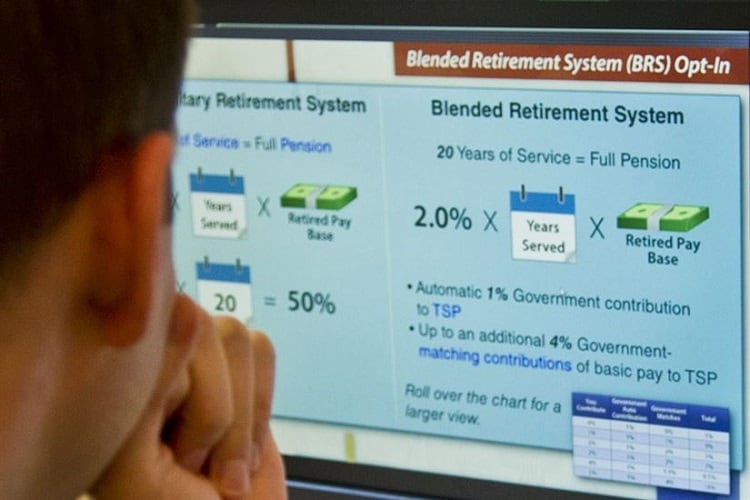

Byington said he didn’t find the calculator tool provided by the Defense Department to be useful, because he couldn’t run all his variables and assumptions at once, so he “took just the facts and known numbers, made some assumptions, and did the math.”

He calculated that if he retires from the military and lives to be 90, the legacy system will pay him between $250,000 and $500,000 more over his lifetime.

Meanwhile, Byington, who is recently divorced, has other life goals.

The 31-year-old, who has almost 10 years of service, wants to be financially independent when he retires from the military, and his goal is to retire around age 44 to 46.

But if he retires in his mid-40s and doesn’t embark on a second career, he wants to be able to bridge the 15-year or so gap between his military retirement and age 59 ½, when he’ll be able to withdraw money from his Thrift Savings Plan account without penalty.

Byington, who is assigned to the Pentagon, is also considering the possibility of buying a house in the mountains and would want to have that house paid off by the time he retires.

He knows he wants children and wants to start saving for their college from the day they’re born.

But it’s not all about the future.

“I’m committed to traveling and living my best life today, after retirement, and in my golden years,” he said.

RELATED

His questions relate to how much money he needs to accumulate and the best way to save and invest that money, assuming he has military retirement pay.

While the numbers are important, a key part of this equation for Byington — and for every service member deciding whether to opt in to the new Blended Retirement System — is the career aspect.

Byington, who is a special agent with the Air Force Office of Special Investigations, is scheduled to be promoted to major on March 1.

He said he’s very hopeful that, if he desires, he’ll be able to continue his service for 20-plus years.

“Right now, they treat me great, and I think I give them what they’re looking for,” he said.

But, financially, he would be okay if he did have to leave the Air Force, he said.

“It would totally change my dreams and my life goals and how I achieve those,” he said. “The Air Force treats me great, but if my life started to suck, I want to have the financial viability to separate.”

Byington has been socking away 15 percent of his basic pay into his Thrift Savings Plan for about three years. He contributed before but in smaller amounts.

RELATED

He and his ex-wife stopped contributing to their retirement funds in 2012 in order to attack their $105,000 in debt, including a car loan, credit card debt and student loan debt. They paid it off in three years.

| Byington snapshot | |

|---|---|

| Blended Retirement System? | No |

| Time in service | 9 1/2 years |

| Income | $110,000/year |

| Consumer debt | 0 |

| Emergency fund | $35,000 |

| Retirement assets | TSP, $70,000 |

Reviewer: JJ Montanaro, a certified financial planner for USAA

Recommendations: Byington’s decision to stick with the legacy retirement system “makes sense in the context of your situation and plans,” Montanaro told Byington. “I think the decision is less about number-crunching than it is about your career plans and glidepath in the military. … You are roughly 10 years into your career, your performance has been good, and your determination to serve 20 years and qualify for retirement benefits make sticking with the legacy system an easy call.

“I do like that you took the time to crunch the numbers and agree with your numerical conclusion given your assumptions.”

Montanaro helped Byington develop a target goal of $2.5 million to accumulate in his TSP to meet his retirement income goals after age 59 ½, when he can start withdrawing the money.

Montanaro said Byington is on the way to accumulating that $2.5 million, depending on assumptions of rates of return on his investments.

As far as filling any possible gap between the time he retires at around age 44 until he’s 59 ½ and can start withdrawing the TSP money, the worst-case scenario would be that he’d need around $600,000 in savings and investments outside the retirement accounts.

And that would only be if he had two house or rent payments for the entire time (i.e., if he bought retirement property before settling there.)

“His military retirement and lack of debt could allow him to get by with significantly less,” Montanaro said.

While it may be difficult for Byington to accumulate enough money to pay off a house before retiring, in addition to his other savings, Montanaro said, he could earmark money for the purpose now, and it could be at least a robust down payment on a house.

Montanaro suggested three different sets of investments: an “emergency/fun today” fund in an accessible account such as a savings account; a retirement account; and “non-retirement” investments he could use to save for the mountain property and to supplement his military retirement income starting in his 40s.

These funds don’t have the limitations that retirement funds do in terms of access before age 59 ½.

Byington already has two of the three types — the emergency/fun today fund and the retirement account.

Currently, Byington is saving and investing 30 percent of his income, which Montanaro describes as “fantastic — well done!”

It’s also great that Byington has no debt.

“This allows you to dedicate your income to what’s important to you!” Montanaro said.

RELATED

What’s next: Byington said he’s gratified that Montanaro validated his decision to stay with the legacy retirement system.

“If I retire from the military, I’ll be just fine until age 44, so we talked about making sure that 15-year gap is covered” before he can start withdrawing money from his TSP, Byington said.

They discussed some possibilities in asset allocation funds, for those non-retirement investments, including some online robo-platforms, which use data algorithms to create automated financial plans.

“I recently opened up an account with one of the several that he listed, after I did some research,” Byington said.

Being debt-free is a critical part of his future retirement plans, he said. Money being paid toward debt, even if it is interest-free debt, could instead be going toward saving for the future.

“People who have any amount of debt, no matter what the interest rate, that hinders them in retiring,” Byington said. “I want to be able to do whatever I want after I’m about 45 years old. And if that means working, that’s fine, too.”

Karen has covered military families, quality of life and consumer issues for Military Times for more than 30 years, and is co-author of a chapter on media coverage of military families in the book "A Battle Plan for Supporting Military Families." She previously worked for newspapers in Guam, Norfolk, Jacksonville, Fla., and Athens, Ga.